Of course, we’re susceptible to hype as well, which is why we asked ChatGPT to write the intro to this article:

Not bad. But, simple curiosity aside, it’s the practical considerations we’ll focus on today. This article serves as an overview of how experts think the markets will move, how trends will develop, and which risks and opportunities to watch over the coming 12 months. Let’s gaze into the crystal ball.

The Economic Vibe Check

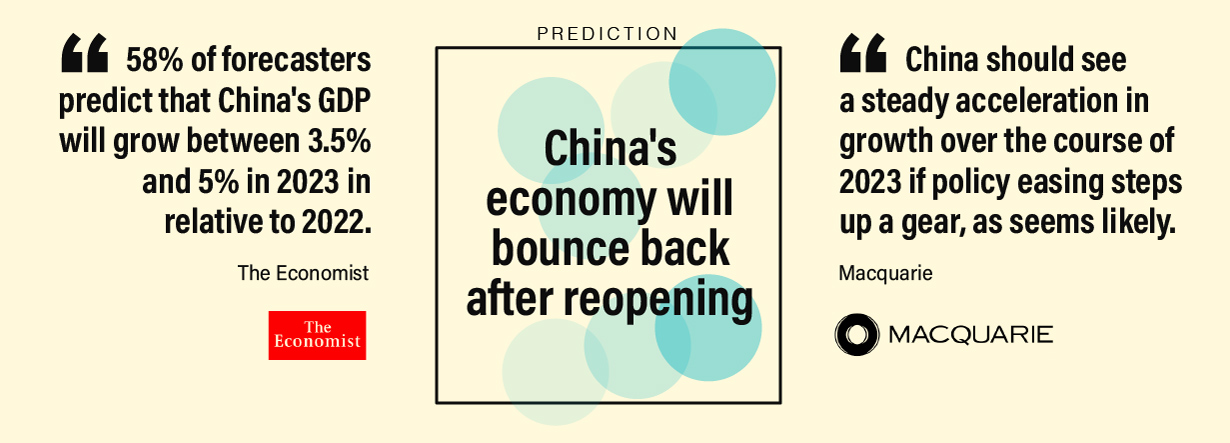

First, we’ll look at some big picture themes, and how experts see them playing out over 2023. Inflation: This was the top economic story of last year, so it’s a natural starting place. Many of the expert opinions in this year’s database (now at 500+ predictions) are pointing to inflation easing off as the year progresses*. On the downside, few predict that inflation will drop back down to the 2% range that Fed policymakers favor. GDP: Forecasters have been revising their economic projections downward in recent weeks. The latest was World Bank, which now sees global growth declining to 1.7% in 2023, down from 3% just six months ago. Most of the predictions in our database see global economic growth in the range of 1.5% to 2%. Recession: As 2022 came to a close, the broad sentiment among experts in the financial industry is that recession is all but inevitable in developed markets this year. As dawn breaks in 2023, a few analysts now feel that the U.S.—and possibly Europe—could narrowly avoid recession. Markets: Experts on Wall Street and beyond are cautiously optimistic about equities, and after the worst year on record for bonds in 2022, most analysts are declaring that “Bonds are back”. *Interestingly, this was also last year’s prediction, but the scale of Russia’s invasion of Ukraine was a curve ball that caught many experts off guard.

AI is Eating the World

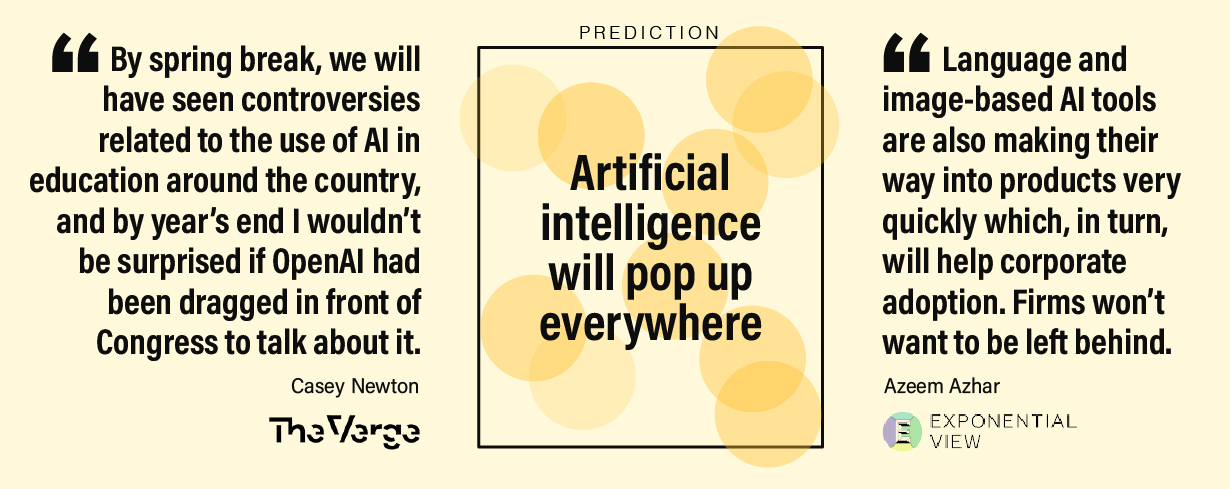

Jobs being displaced by automation is far from a new theme, but given the exponential improvements in AI in recent years, the risk to entire industries feels more existential today. As an example, let’s consider art and design. One of the ways many illustrators and artists earn a living is through commissions—essentially being hired and paid to create a specific piece of art in their style. Today though, free, powerful AI tools, such as Midjourney, allow users to generate high-quality art in an infinite number of styles with just a few clicks. Real art will never truly go out of style, and accomplished artists will always attract an audience, but this one example shows how quickly technology can disrupt an industry. (Artists can take solace in the fact that AI is still comically bad at rendering hands.)

Of course, there are obvious positive aspects to this technological advancement as well. Generative AI tools are useful for generating ideas and mock-ups, and even functional snippets of code. AI systems like AlphaFold unlock a world of possibilities in scientific domains. From the hundreds of predictions we evaluated, it’s clear that experts view AI as a major catalyst this year. AI start-ups are forcing Big Tech to innovate faster, and employees are finding new ways to use AI-powered tools to increase productivity. Experts predict that AI will impact peoples’ lives in a much more visible and tangible way in 2023 than in past years.

The China Factor

As world’s second largest economy and linchpin of global trade, events in China have a major impact on the world economy. Xi Jinping’s reversal of Zero-COVID restrictions should drastically change the trajectory of the country’s economy. For one, reopening will unleash a flood of household spending and consumption.

China’s reopening will also impact other economies as well. For example, the resumption of travel will be a boon to destinations favored by Chinese vacationers. Economically, Hong Kong stands to benefit immensely—its GDP could jump upwards of 8% after reopening is complete. Emerging market commodity exporters could see a lift as well, though inflation could be reinvigorated as a result. In the U.S., a storm is brewing over the extremely popular video app, TikTok. Many experts predict that regulators will either ban the app altogether in 2023, or force the sale of the company to an American entity. Regardless how that situation plays out, it underscores the souring relationship between the U.S. and China. The rivalry will continue to have ripple effects on the global markets throughout the year.

Energy

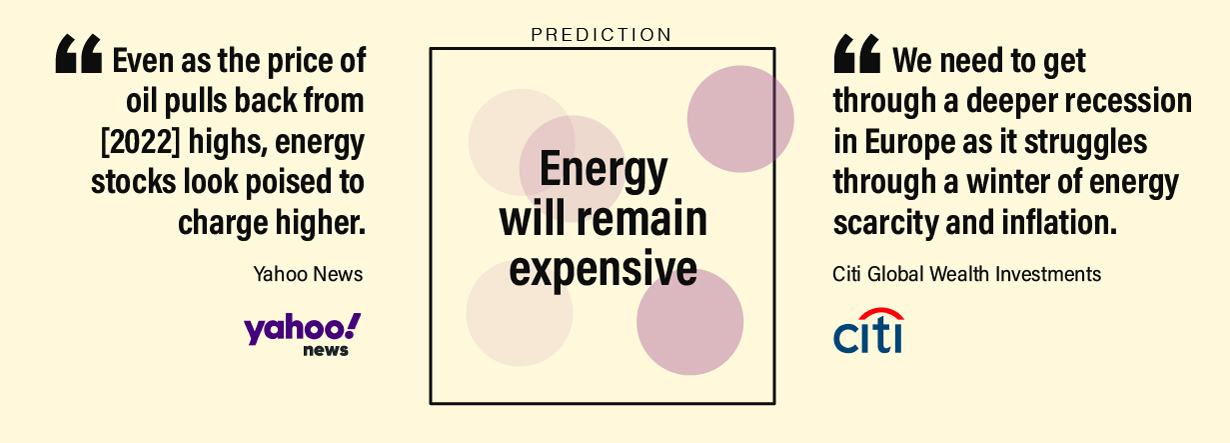

Energy was the S&P 500’s top performing sector two years in a row, and many experts feel that more growth is on the horizon. The global system that supplies us with energy is breathtakingly complex, with a lot of unpredictable factors at play. Of all factors, conflict can create the most volatility, and 2023 has a number of geopolitical risks that could impact energy supplies. First, Europe will continue to diversify its energy imports away from Russia. Recently, liquefied natural gas from the U.S. has helped fill gaps.

Next, Iran could be a flashpoint in the Middle East this year. A brewing conflict in the region could cause instability, which will have knock-on effects on the energy industry—particularly in the event of attacks on oil and gas infrastructure. Here are a few other factors to consider this coming year:

The U.S. Energy Department will aim to replenish its Strategic Petroleum Reserve Easing of U.S. sanctions on Venezuela could lay the ground work for increased oil production In post-Zero-COVID China, economic activity will increase, pushing up demand In the UK, the energy price guarantee will rise in April, meaning higher energy bills for households

The Elon Playbook

After a lull in December (nobody wants to be the company that fires people during the holiday season) tech and tech-adjacent companies have resumed their zealous slashing of headcounts. Given the influence of Elon Musk in the tech industry, many experts are suggesting that his strategy of ruthlessly slashing headcount at Twitter might serve as inspiration for other technology leaders.

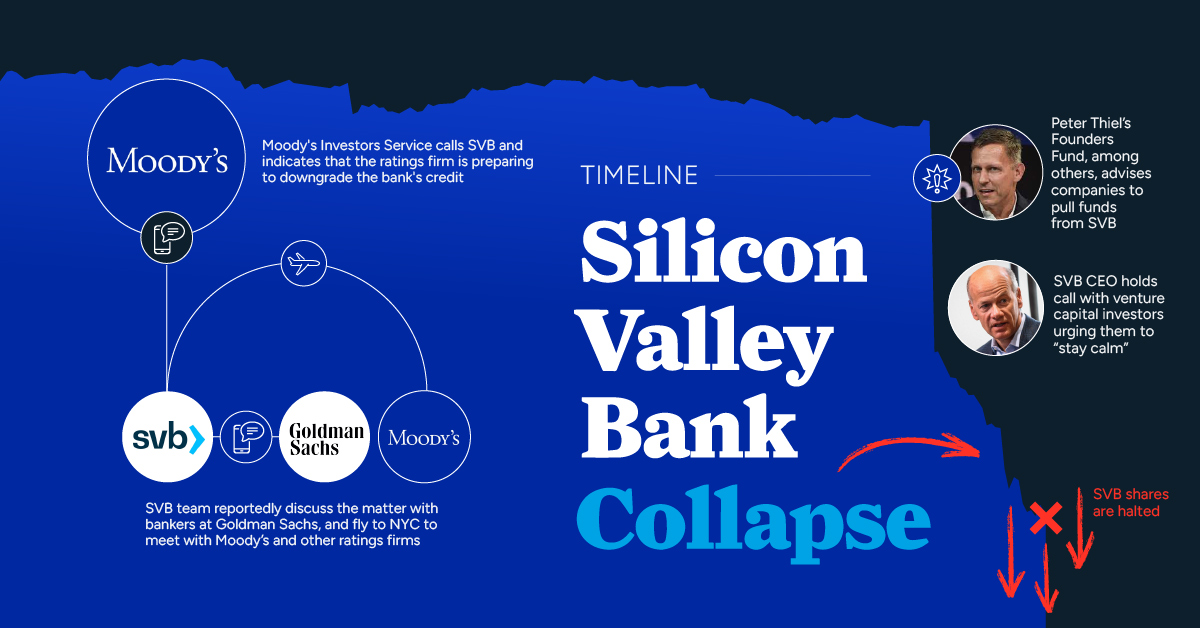

Employees in the tech industry are very well compensated, and many were hired during periods of intense competition between companies to attract talent and capture market share. During a downturn, it’s tempting—and often necessary—for companies to course-correct. There were also predictions that the whole start-up and investment ecosystem could be switching from a hypergrowth to a value-focused mindset, which is a theme that is worth consideration in 2023. on But fast forward to the end of last week, and SVB was shuttered by regulators after a panic-induced bank run. So, how exactly did this happen? We dig in below.

Road to a Bank Run

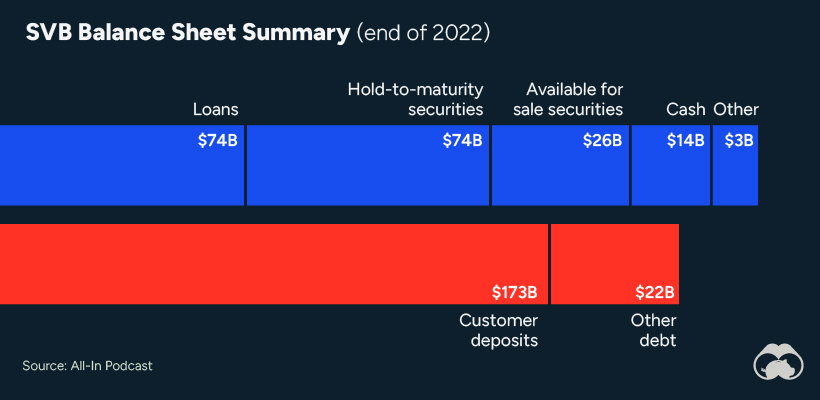

SVB and its customers generally thrived during the low interest rate era, but as rates rose, SVB found itself more exposed to risk than a typical bank. Even so, at the end of 2022, the bank’s balance sheet showed no cause for alarm.

As well, the bank was viewed positively in a number of places. Most Wall Street analyst ratings were overwhelmingly positive on the bank’s stock, and Forbes had just added the bank to its Financial All-Stars list. Outward signs of trouble emerged on Wednesday, March 8th, when SVB surprised investors with news that the bank needed to raise more than $2 billion to shore up its balance sheet. The reaction from prominent venture capitalists was not positive, with Coatue Management, Union Square Ventures, and Peter Thiel’s Founders Fund moving to limit exposure to the 40-year-old bank. The influence of these firms is believed to have added fuel to the fire, and a bank run ensued. Also influencing decision making was the fact that SVB had the highest percentage of uninsured domestic deposits of all big banks. These totaled nearly $152 billion, or about 97% of all deposits. By the end of the day, customers had tried to withdraw $42 billion in deposits.

What Triggered the SVB Collapse?

While the collapse of SVB took place over the course of 44 hours, its roots trace back to the early pandemic years. In 2021, U.S. venture capital-backed companies raised a record $330 billion—double the amount seen in 2020. At the time, interest rates were at rock-bottom levels to help buoy the economy. Matt Levine sums up the situation well: “When interest rates are low everywhere, a dollar in 20 years is about as good as a dollar today, so a startup whose business model is “we will lose money for a decade building artificial intelligence, and then rake in lots of money in the far future” sounds pretty good. When interest rates are higher, a dollar today is better than a dollar tomorrow, so investors want cash flows. When interest rates were low for a long time, and suddenly become high, all the money that was rushing to your customers is suddenly cut off.” Source: Pitchbook Why is this important? During this time, SVB received billions of dollars from these venture-backed clients. In one year alone, their deposits increased 100%. They took these funds and invested them in longer-term bonds. As a result, this created a dangerous trap as the company expected rates would remain low. During this time, SVB invested in bonds at the top of the market. As interest rates rose higher and bond prices declined, SVB started taking major losses on their long-term bond holdings.

Losses Fueling a Liquidity Crunch

When SVB reported its fourth quarter results in early 2023, Moody’s Investor Service, a credit rating agency took notice. In early March, it said that SVB was at high risk for a downgrade due to its significant unrealized losses. In response, SVB looked to sell $2 billion of its investments at a loss to help boost liquidity for its struggling balance sheet. Soon, more hedge funds and venture investors realized SVB could be on thin ice. Depositors withdrew funds in droves, spurring a liquidity squeeze and prompting California regulators and the FDIC to step in and shut down the bank.

What Happens Now?

While much of SVB’s activity was focused on the tech sector, the bank’s shocking collapse has rattled a financial sector that is already on edge.

The four biggest U.S. banks lost a combined $52 billion the day before the SVB collapse. On Friday, other banking stocks saw double-digit drops, including Signature Bank (-23%), First Republic (-15%), and Silvergate Capital (-11%).

Source: Morningstar Direct. *Represents March 9 data, trading halted on March 10.

When the dust settles, it’s hard to predict the ripple effects that will emerge from this dramatic event. For investors, the Secretary of the Treasury Janet Yellen announced confidence in the banking system remaining resilient, noting that regulators have the proper tools in response to the issue.

But others have seen trouble brewing as far back as 2020 (or earlier) when commercial banking assets were skyrocketing and banks were buying bonds when rates were low.