Over the past 20 years, gold mining stocks have outperformed the price of gold bullion in bull markets, offering what can be seen as a leveraged play on gold’s price appreciation. While gold miners offer more potential upside, they also have higher volatility and greater downside during dips, making market timing and strong hands all the more important. This infographic comes to us from Sprott and compares the returns of gold stocks and gold bullion in bull markets. It also explains how gold stocks outperform thanks to profit expansion, and shows why there might be more upside for gold miners to come.

How Operating Leverage Benefits Gold Mining Companies

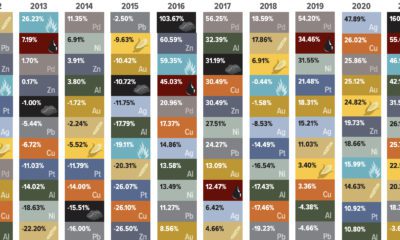

During the 2000-2011 gold bull market, the price of physical gold rose 550%. While you might think that number is hard to beat, over the same period of time gold mining equities (represented by the NYSE Arca Gold Miners Index) returned more than 690%.

In the current gold bull market which started in 2015, gold mining stocks are up more than 182%, more than doubling gold bullion’s 78% returns.

This outperformance in bull markets is largely due to how gold mining companies use their operating leverage to maximize profits, resulting in their share prices appreciating.

Breaking Down Gold Mining Costs and Profits

As a gold mining company mines and produces gold, the gold is sold on the market fairly quickly to avoid the risk of gold’s price depreciating. When the price of gold rises, miners immediately start to see greater profits from selling their ounces on the market. While the costs to mine gold also rise in bull markets, they rise less and at a slower rate. The result of this is profit expansion: when operationally efficient gold mining companies are able to capture larger profits, resulting in increased operating and free cash flow.

Breakdown of Barrick Gold’s Profit per Ounce of Gold

During the current gold bull run which started in 2015, Barrick Gold’s average realized price per troy ounce of gold increased by 50%, while their all-in sustaining costs per troy ounce only went up by 18%. This has resulted in the company increasing their profit per ounce of gold sold by a staggering 134% over the past six years.

Making the Most of Golden Times

While higher profit margins during bull markets are great, it’s up to the individual company to ensure the extra cash is being used prudently to efficiently support their operations.

Bull markets don’t last forever, and gold miners must use these prosperous times to strengthen their balance sheets, reward shareholders, and reinvest into projects which will provide future value and returns.

Dividend-paying gold stocks increase dividends to reward loyal shareholders, with the average dividend increase of top gold mining stocks in a bull market often doubling.

Over the decades, companies have gotten better at making the most of bull markets in order to be well-guarded for when gold prices stop appreciating, and eventually start declining.

Why Gold Mining Stocks May Still Be Undervalued

Even if gold mining stocks have already seen impressive returns over the past five years, there are some technical indicators which point to them still being undervalued compared to other equities and gold bullion.

The top 10 gold mining companies have seen their earnings per share estimates almost triple in the past two years. The top 20 S&P 500 companies have seen around a -15% decline in their earnings per share estimates.

Along with having better earnings per share compared to the top U.S. equities, gold mining stocks may also be undervalued compared to gold bullion. The gold mining stocks to gold bullion ratio is at historically low levels after having dropped more than 60% following the 2008 financial crisis. While gold bullion is increasingly seen as a safe haven asset for investors, gold miners are still overlooked despite their strong technicals.

Gold and Gold Miners’ Role in the Future Economy

As money printing has been the Federal Reserve’s main answer to an increasingly volatile economic climate, gold and its producers are set to play a crucial role in helping investors preserve their wealth.

Gold has yet again outperformed just about every other asset class in 2020, and gold miners offer even greater returns for those willing to manage the additional risk they present.

Gold mining stocks are much more volatile compared to gold bullion, and have a variety of additional risks dependent on their company structure, jurisdiction of operations, and operational efficiency. But for investors who are looking for exceptional returns in gold bull markets, they can be an alluring option.

on

Did you know that nearly one-fifth of all the gold ever mined is held by central banks?

Besides investors and jewelry consumers, central banks are a major source of gold demand. In fact, in 2022, central banks snapped up gold at the fastest pace since 1967.

However, the record gold purchases of 2022 are in stark contrast to the 1990s and early 2000s, when central banks were net sellers of gold.

The above infographic uses data from the World Gold Council to show 30 years of central bank gold demand, highlighting how official attitudes toward gold have changed in the last 30 years.

Why Do Central Banks Buy Gold?

Gold plays an important role in the financial reserves of numerous nations. Here are three of the reasons why central banks hold gold:

Balancing foreign exchange reserves Central banks have long held gold as part of their reserves to manage risk from currency holdings and to promote stability during economic turmoil. Hedging against fiat currencies Gold offers a hedge against the eroding purchasing power of currencies (mainly the U.S. dollar) due to inflation. Diversifying portfolios Gold has an inverse correlation with the U.S. dollar. When the dollar falls in value, gold prices tend to rise, protecting central banks from volatility. The Switch from Selling to Buying In the 1990s and early 2000s, central banks were net sellers of gold. There were several reasons behind the selling, including good macroeconomic conditions and a downward trend in gold prices. Due to strong economic growth, gold’s safe-haven properties were less valuable, and low returns made it unattractive as an investment. Central bank attitudes toward gold started changing following the 1997 Asian financial crisis and then later, the 2007–08 financial crisis. Since 2010, central banks have been net buyers of gold on an annual basis. Here’s a look at the 10 largest official buyers of gold from the end of 1999 to end of 2021: Rank CountryAmount of Gold Bought (tonnes)% of All Buying #1🇷🇺 Russia 1,88828% #2🇨🇳 China 1,55223% #3🇹🇷 Türkiye 5418% #4🇮🇳 India 3956% #5🇰🇿 Kazakhstan 3455% #6🇺🇿 Uzbekistan 3115% #7🇸🇦 Saudi Arabia 1803% #8🇹🇭 Thailand 1682% #9🇵🇱 Poland1282% #10🇲🇽 Mexico 1152% Total5,62384% Source: IMF The top 10 official buyers of gold between end-1999 and end-2021 represent 84% of all the gold bought by central banks during this period. Russia and China—arguably the United States’ top geopolitical rivals—have been the largest gold buyers over the last two decades. Russia, in particular, accelerated its gold purchases after being hit by Western sanctions following its annexation of Crimea in 2014. Interestingly, the majority of nations on the above list are emerging economies. These countries have likely been stockpiling gold to hedge against financial and geopolitical risks affecting currencies, primarily the U.S. dollar. Meanwhile, European nations including Switzerland, France, Netherlands, and the UK were the largest sellers of gold between 1999 and 2021, under the Central Bank Gold Agreement (CBGA) framework. Which Central Banks Bought Gold in 2022? In 2022, central banks bought a record 1,136 tonnes of gold, worth around $70 billion. Country2022 Gold Purchases (tonnes)% of Total 🇹🇷 Türkiye14813% 🇨🇳 China 625% 🇪🇬 Egypt 474% 🇶🇦 Qatar333% 🇮🇶 Iraq 343% 🇮🇳 India 333% 🇦🇪 UAE 252% 🇰🇬 Kyrgyzstan 61% 🇹🇯 Tajikistan 40.4% 🇪🇨 Ecuador 30.3% 🌍 Unreported 74165% Total1,136100% Türkiye, experiencing 86% year-over-year inflation as of October 2022, was the largest buyer, adding 148 tonnes to its reserves. China continued its gold-buying spree with 62 tonnes added in the months of November and December, amid rising geopolitical tensions with the United States. Overall, emerging markets continued the trend that started in the 2000s, accounting for the bulk of gold purchases. Meanwhile, a significant two-thirds, or 741 tonnes of official gold purchases were unreported in 2022. According to analysts, unreported gold purchases are likely to have come from countries like China and Russia, who are looking to de-dollarize global trade to circumvent Western sanctions.

There were several reasons behind the selling, including good macroeconomic conditions and a downward trend in gold prices. Due to strong economic growth, gold’s safe-haven properties were less valuable, and low returns made it unattractive as an investment.

Central bank attitudes toward gold started changing following the 1997 Asian financial crisis and then later, the 2007–08 financial crisis. Since 2010, central banks have been net buyers of gold on an annual basis.

Here’s a look at the 10 largest official buyers of gold from the end of 1999 to end of 2021:

Source: IMF

The top 10 official buyers of gold between end-1999 and end-2021 represent 84% of all the gold bought by central banks during this period.

Russia and China—arguably the United States’ top geopolitical rivals—have been the largest gold buyers over the last two decades. Russia, in particular, accelerated its gold purchases after being hit by Western sanctions following its annexation of Crimea in 2014.

Interestingly, the majority of nations on the above list are emerging economies. These countries have likely been stockpiling gold to hedge against financial and geopolitical risks affecting currencies, primarily the U.S. dollar.

Meanwhile, European nations including Switzerland, France, Netherlands, and the UK were the largest sellers of gold between 1999 and 2021, under the Central Bank Gold Agreement (CBGA) framework.

Which Central Banks Bought Gold in 2022?

In 2022, central banks bought a record 1,136 tonnes of gold, worth around $70 billion. Türkiye, experiencing 86% year-over-year inflation as of October 2022, was the largest buyer, adding 148 tonnes to its reserves. China continued its gold-buying spree with 62 tonnes added in the months of November and December, amid rising geopolitical tensions with the United States. Overall, emerging markets continued the trend that started in the 2000s, accounting for the bulk of gold purchases. Meanwhile, a significant two-thirds, or 741 tonnes of official gold purchases were unreported in 2022. According to analysts, unreported gold purchases are likely to have come from countries like China and Russia, who are looking to de-dollarize global trade to circumvent Western sanctions.